A Radical Shift in Youth Money Management

The youngest members of the workforce are the only ones causing a significant disturbance to the global financial scene. The norms of personal finance are being fundamentally rewritten by Generation Z, according to recent macroeconomic statistics from key institutions. In an effort to overcome severe economic challenges, this dynamic group openly rejects the customary, clandestine financial practices of earlier generations. As a result, economists, retail banks, and consumer brands around the world now need to comprehend the most recent Gen Z budgeting tendencies.

Despite significant daily cash flow issues, new corporate intelligence reveals a startling move toward independent money management. For instance, a significant decrease in family financial dependence is revealed by the extensive Bank of America Better Money Habits survey. Just two years ago, 46% of young people received financial support from their parents; today, only 34% do. Young workers’ desire for complete control over their financial futures is demonstrated by this quick shift toward self-sufficiency.

These young people’s independence does not, however, imply that they have a lot of extra money or profitable professional options. According to the research, because of ongoing inflation, 42% of this generation today lives paycheck to paycheck. 49% of respondents cited the overall cost of living as a hindrance, while high housing expenses and exorbitant grocery prices continue to be significant challenges. However, rather than giving up, many customers use innovative, digital-first tactics to create long-lasting personal savings.

Deconstructing Loud Budgeting and Radical Transparency

Loud budgeting, a social media phenomena that has gone global, is the most obvious example of contemporary financial practices. Customers are encouraged by this behavioral tendency to publicly state which social events they cannot afford and to reject peer pressure. Young adults today view financial boundaries as a mark of maturity and integrity rather than as a way to conceal financial difficulty. 42% of Gen Z publicly engage in loud budgeting with friends and family, according to research.

Decades of rigid social taboos about personal income, debt levels, and lifestyle restrictions have been broken by this extreme transparency. 60% of young workers regularly have entirely honest conversations about money with their main social groups. They frequently talk about delicate subjects including precise pay amounts, monthly rent expenses, and debt-related emotional anguish.

Additionally, this transparency directly affects consumer purchasing decisions within local economies, weekend group plans, and daily social behavior. When making arrangements with friends, almost 75% of young adults actively and consciously try to save money. Typical strategies include purchasing less expensive dining items, organizing informal get-togethers at their homes, or recommending free public events. Individual bank accounts are safeguarded by this common cost-conscious mindset, which also eliminates the stigma attached to saving money.

The Death of the Luxury Date and Intrepid Frugality

The current state of romance and interpersonal relationships has been drastically altered by the constant pressure on daily financial flow. A growing number of young singles see extravagant first dates or careless spending as serious behavioral warning signs in possible mates. Recent consumer studies show that 74% of participants want a long-term love partner to be financially responsible. On the other hand, 43% believe that careless personal spending is an instant, non-negotiable relationship breakdown.

| GEN Z SOCIAL SAVING STRATEGIES | ||

| STRATEGY TYPE | POPULATION ADOPTION | PRIMARY ECONOMIC BENEFIT |

| Cheap/Free Plans Budget Ordering Pre-Eating At Home | 39% of Gen Z 38% of Gen Z 31% of Gen Z | Eliminates Event Entry Costs Reduces Restaurant Tabs Lowers Overall Food Costs |

| Source: Bank of America Better Money Habits Financial Study (2026) | ||

The zero-dollar romantic date option is a result of this rigorous monitoring of peer spending patterns. At the moment, half of all young individuals questioned spend precisely zero dollars on formal dating events each month. While some people just don’t date at all, 15% openly say they can’t afford the expense of romance. In addition, about 25% of this group expressly postpones advancing partnerships because of severe financial anxiety.

When these people do spend money, they give priority to high-frequency necessities above large, opulent lifestyle items. Financial processors’ transaction data shows a strong concentration in quick-service restaurants, big-box stores, and regular grocery shopping. In order to preserve their vital daily financial reserves, young customers voluntarily reduce their spending on pricey vacation reservations. In their social groups, this pragmatic approach prioritizes long-term survival over transient, surface-level status symbols.

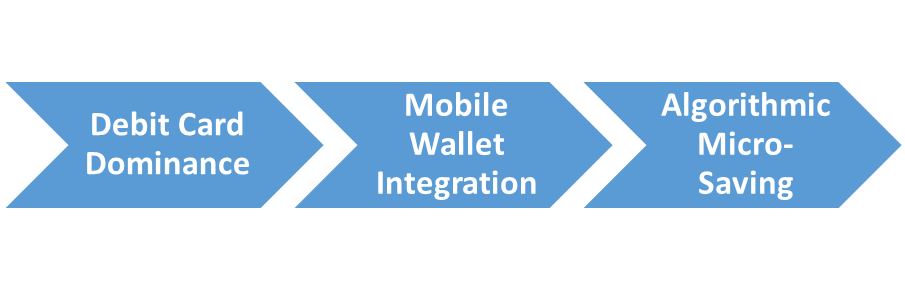

Digital Innovation and the Proliferation of Alternative Payments

The quick implementation of these contemporary cash-tracking techniques is made possible by technology, which is indispensable. These customers anticipate smooth, quick, and completely cashless mobile banking encounters because they grew up with the internet. They view smartphone apps as essential counselors for everyday wealth growth, rather than merely as standard tools. To explore the global rise of financial technology platforms, consult the Deloitte Global Financial Services Insights Portal.

In response, fintech companies have incorporated budgeting trackers and highly automated micro-saving tools into their normal user interfaces. Furthermore, Buy Now, Pay Later platforms and other alternative payment methods have become widely accepted. Every week, about one in five young customers use programs for interest-free installment payments. For necessary expenditures like business attire or college textbooks, this payment option offers vital liquidity management.

However, because of their reliance on digital infrastructure, young investors are also exposed to hazardous, unregulated financial advice online. Instead of traditional financial consultants, millions of young people turn to producers of short-form video content for investment advice. This behavior has caused speculative asset ownership among inexperienced retail market players to soar. For instance, this group’s cryptocurrency ownership was in the single digits just three years ago; today, it is at 23%.

Editor’s Perspective: The Triumphant Realism of a Realistic Generation

These aggressive Gen Z budgeting practices, in my opinion, are a great and essential reaction to systemic economic failure. When talking about working practices and corporate goals, older critics often accuse this generation of being entitled or hypersensitive. However, the empirical evidence presents an entirely different picture of extreme survival, pragmatism, and fortitude. With astounding intellectual honesty, young folks must deal with excessive inflation and exorbitant housing costs.

The widespread use of loud budgeting demonstrates that younger people are more financially responsible than older generations. Open conversations about salaries and savings were considered profoundly inappropriate or unpleasant by polite society for decades. Wages remained low and consumer debt levels remained dangerously high as a result of that corporate-backed deception. These employees are methodically destroying the exploitative mentality of maintaining appearances by being open about financial constraints.

I believe that corporate retail and traditional banking will undergo significant structural changes as a result of this extreme financial realism. A generation that appreciates debit rails cannot be sold complicated, high-interest credit products by financial firms. Over the next ten years, brands that depend on unthinking customer impulse buying will experience significant revenue losses. Before spending money, young consumers need genuine ethical alignment, transparent pricing mechanisms, and actual value.

Furthermore, significant societal milestones like family planning and homeownership will unavoidably change as a result of this financial lockout. Due to young people’s refusal to take on toxic debt, we are seeing a record delay in traditional adult milestones. Before growing their houses, many would rather live with their parents or roommates to protect their personal finances. This deliberate prudence is a skillful demonstration of economic self-defense rather than a show of weakness.

Balancing the Little Treat Culture with Financial Guilt

Young consumers are fiercely committed to thrift, but they won’t completely give up their happiness in favor of an austere lifestyle. Instead, they engage in a complex kind of financial gymnastics to strike a balance between short-term enjoyment and long-term objectives. The little treat culture, in which consumers treat themselves to modest, reasonably priced everyday indulgences, has gained popularity as a result of this behavior. At least once a week, 92% of young adults acknowledge making little impulsive purchases.

Specialty iced coffees, fine pastries, or low-cost cosmetics like lip balms are examples of these reasonably priced delights. Customers live extremely frugally during the workweek in order to pay for these little pleasures without blowing their budgets. To enjoy their weekend social plans guilt-free, they voluntarily prepare simple meals at home for days. This well-rounded strategy offers the required emotional respite without necessitating the relinquishment of ultimate financial authority.

But this ongoing balancing act also causes a great deal of emotional anguish and consumer regret each week. After making discretionary purchases, nearly 41% of young consumers say they experience severe financial remorse right away. Forty percent of consumers want rapid approval from close friends or family members after purchasing in order to counteract this unpleasant reaction. The psychological toll of navigating a high-cost economy in early adulthood is highlighted by this study.

The Road Ahead for Youth Wealth Accumulation

The ability of young people to turn short-term savings into investments will have a significant impact on their long-term wealth accumulation prospects. An astounding 66% of this group successfully saves money each month despite confronting unprecedented economic challenges. They accomplish this by automatically allocating any remaining funds to employer-sponsored retirement plans or high-yield savings accounts. As they approach their prime earning years, this steady discipline bodes incredibly well for their future financial security.

- Automate Paycheck Deductions: As soon as each paycheck is received, a predetermined portion of it is transferred into different investing accounts.

- Verify Social Media Advice: Before putting money at risk, compare popular online financial advice with reliable, trustworthy sources.

- Leverage Workplace Matching: To fully benefit from free employer-matching funds, maximize contributions to business 401(k) plans.

- Audit Subscription Services: To get rid of unused streaming or gaming apps, examine recurring digital monthly fees on a regular basis.

In the end, this emerging economic powerhouse’s fiercely independent character will not be broken by unfriendly macroeconomic factors. These people are laying a firm basis through digital innovation, radical openness, and meticulous spending tracking. They are demonstrating that genuine financial freedom necessitates having the guts to live within one’s means. The inevitable growth of financial realism has formally put an end to the period of performative consumer spending.

Leave a Reply